This article was originally published in Postnoon on September 9th, 2012

http://postnoon.com/2012/09/07/understanding-emis/71082

A week after our first set of discussions about home loans, Abhi came back to me for further assistance with understanding home loans. He told me that he had approached his bank and started the process of getting a loan sanctioned. He had already submitted self attested copies of four months pay slips, six months' salary bank statements, past three years Form 16s, ID proof, address proof, PAN Card and the employee ID.

Abhi: Nicky, tell me, what are EMIs and how are they calculated?

Nicky: Equated Monthly Installment or EMI, as they are popularly known as, is a fixed amount of money that you return to the bank, on a specific date of each month. The EMI consists of part repayment of principal and the interest. It is calculated in such a way that over a period of time, if you pay all the EMIs on time, your loan will get completely repaid.

Abhi: Why don't we just pay the interest every month and repay the principal after the term of the loan is over?

Nicky: Well, you could do that. But that would mean that you pay interest on the entire principal throughout the term. Also, when the term gets over, you may not have enough money to repay the principal. In EMIs, because you are also repaying a part of the principal every month, the interest component keeps decreasing every month. Every month, you pay interest on a lesser principal.

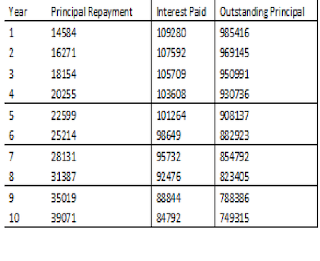

Another advantage is that the principal repayment is spread over many months, typically 240 or 120 months, relieving you of the burden of paying a very large amount at one time in the end. For example, if you were to take a loan of Rs10 lakhs at an interest of 11%, you will need to pay an EMI of Rs10,322 per month. This is equal to Rs1,23,864 per annum. If you look at the Table, you can clearly see that every year, your payment towards interest is coming down, as the interest is calculated only on the balance of the principal amount. If you keep paying Rs10,322 every month, for 20 years, you would have cleared your entire loan, along with all the interest.

Year Principal Repayment Interest Paid Outstanding Principal

Abhi: That's very comforting.

Abhi: That's very comforting.

Nicky: And that's not all. You can also avail of tax benefits on both the principal as well as the interest paid.

Abhi: Hmmm...I just wish that my sanction letter comes soon and we are able to move into our new home as soon as possible!

http://postnoon.com/2012/09/07/understanding-emis/71082

A week after our first set of discussions about home loans, Abhi came back to me for further assistance with understanding home loans. He told me that he had approached his bank and started the process of getting a loan sanctioned. He had already submitted self attested copies of four months pay slips, six months' salary bank statements, past three years Form 16s, ID proof, address proof, PAN Card and the employee ID.

Abhi: Nicky, tell me, what are EMIs and how are they calculated?

Nicky: Equated Monthly Installment or EMI, as they are popularly known as, is a fixed amount of money that you return to the bank, on a specific date of each month. The EMI consists of part repayment of principal and the interest. It is calculated in such a way that over a period of time, if you pay all the EMIs on time, your loan will get completely repaid.

Abhi: Why don't we just pay the interest every month and repay the principal after the term of the loan is over?

Nicky: Well, you could do that. But that would mean that you pay interest on the entire principal throughout the term. Also, when the term gets over, you may not have enough money to repay the principal. In EMIs, because you are also repaying a part of the principal every month, the interest component keeps decreasing every month. Every month, you pay interest on a lesser principal.

Another advantage is that the principal repayment is spread over many months, typically 240 or 120 months, relieving you of the burden of paying a very large amount at one time in the end. For example, if you were to take a loan of Rs10 lakhs at an interest of 11%, you will need to pay an EMI of Rs10,322 per month. This is equal to Rs1,23,864 per annum. If you look at the Table, you can clearly see that every year, your payment towards interest is coming down, as the interest is calculated only on the balance of the principal amount. If you keep paying Rs10,322 every month, for 20 years, you would have cleared your entire loan, along with all the interest.

Year Principal Repayment Interest Paid Outstanding Principal

Nicky: And that's not all. You can also avail of tax benefits on both the principal as well as the interest paid.

Abhi: Hmmm...I just wish that my sanction letter comes soon and we are able to move into our new home as soon as possible!

No comments:

Post a Comment