This article was first published in the IIB Bulletin, 2015, Vol. 1, Iss. 3, pp10-12

https://iib.gov.in/IRDA/Articles/IIB%20Bulletin%20Q3%202014-15.pdfCo-Author: Pushpendra Johari (RMSI Private Limited)

Images of destruction caused by the Uttarakhand Floods,

Cyclone Hudhud or the Bhuj Earthquake are still livid in the minds of most of

us. While loss of lives and property are always painful, the scale of

destruction during a natural disaster hits us with a sense of despair at the

helplessness of human beings. Advances in technology and development in economy

could not prevent the Tsunami or the Katrina.

India is prone to natural disasters due to its climate and

topography. As per the research done by Mishra (2014) during the past 100 years

(1913-2013), 51.4 percent of the natural disasters in India were due to floods,

32.7 percent from storms, 7.4 percent from landslides, 5.6 percent from

earthquakes and 2.9 percent from droughts.

The economic losses to the nation are huge; to give a

perspective, in a report in 2003, World Bank estimated that the Economic losses

to India due to natural disasters were around 2 percent of the Gross Domestic

Product (GDP), per annum.

“Reported direct

losses on public and private economic infrastructure in India have amounted to

approximately $30 billion over the past 35 years [up to 2001] (nominal values

at then applying exchange rates). Since less than 25% of the registered loss

events actually provide any loss estimates, the official numbers substantially

understate the true economic impact of direct losses. A crude grossing up for

reporting frequency indicates that direct natural disasters losses equate to up

to 2% of India's GDP and up to 12% of federal government revenues”...Pg 8, The

World Bank Report (2003).

The stakes could be as high as 4.4% and 6.5% of the States

GDP in states like Gujarat and Orissa. The report also noted that the official

figures are generally lower than the actual losses and it also observed a

rising trend in the losses over the years. It must also be noted that these

figures do not include the cost of rehabilitation and restoration.

According to a report on “Natural Hazards, UnNatural

Disasters” by the World Bank and the United Nations, the impact of natural

disasters on the GDP is 20 times higher in developing countries than in industrialized

nations.

The years 2013 and 2014 have seen catastrophes like the

Uttarakhand Floods and the Cyclone Hudhud, which have resulted in large losses,

both of lives and property (Table 1).

Event

|

No. Killed

|

No. Total Affected

|

~Economic Losses

(in Rs crores)

|

~Insured Losses

(in Rs crores)

|

Uttarakhand

Floods

|

6054

|

504473

|

6600

|

3000*

|

Cyclone

Phailin

|

47

|

13230000

|

3800

|

600*

|

Cyclone

Hudhud

|

109

|

10000000*

|

65000*

|

4000*

|

Source: EM-DAT: The OFDA/CRED International

Disaster Database

*Estimate based on news reports

The irony is

that the General Insurance penetration in India is very low, especially for

personal property. The gap between people who need Insurance most and the

penetration of Insurance amongst them is huge. The pace at which the economy of

India is growing is indicative of a huge potential for increasing the insurance

penetration.

The

government of India is desirous to make Insurance as the primary mechanism for

disaster risk financing in India (Ref. Disaster Relief and Risk Transfer

through Insurance, IRDA-NDMA July 2013). A panel including NDMA, IRDA and

general insurers in India is considering several options including:

·

Setting up a pool for states, NDRF, etc.

·

Parametric insurance solutions for NDRF

·

Optional simple Indian Natural Catastrophe

Insurance Policy

·

Mandatory property insurance in highly prone urban

areas

However,

there are several questions that need to be answered before such schemes could

be launched. Some of these questions are:

·

How much fund is needed for the pool

·

Who would fund the pool

·

Categories of population to be covered under the

Indian Natural Catastrophe Insurance policy

·

How to price the coverage of such policies

·

What should be the triggers and how much payment

should be associated to specific triggers for parametric insurance solutions,

etc.

Natural Catastrophe

modelling is the science that can help in finding the answers to several of

these questions.

Probabilistic NatCat modelling can be

used to arrive at the possible economic loss scenarios associated to various

return periods, the impact of specific historical or latest hazard events, as

well as the average annual direct economic loss by state or any other

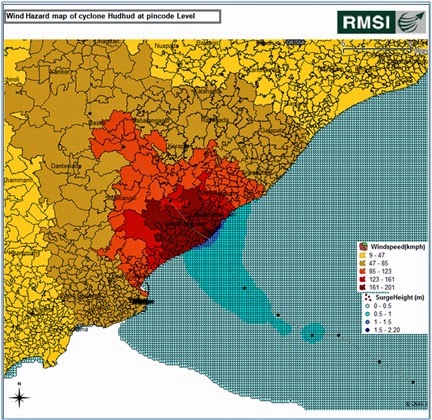

resolution at which the pool needs to be setup. Figure 1 shows the impact of cyclone Hudhud based on RMSI

CycloneRIsk Model.

Figure 1: Cyclone Hudhud wind and surge estimates using RMSI’s

CycloneRIsk model.

Based on return period scenarios various

categories of population that are under high risk zones could be estimated.

Return period losses and average annual loss could be estimated for all these

population categories thereby giving insights into the coverage pricing for

various population categories. Based on the income levels and sample surveys eliciting

willingness to pay for various population categories, an estimate of insurance

affordability could be arrived at. This information could be combined with the

NatCat modelled loss estimates to decide if the entire burden of the insurance

could be passed to any specific population category or not.

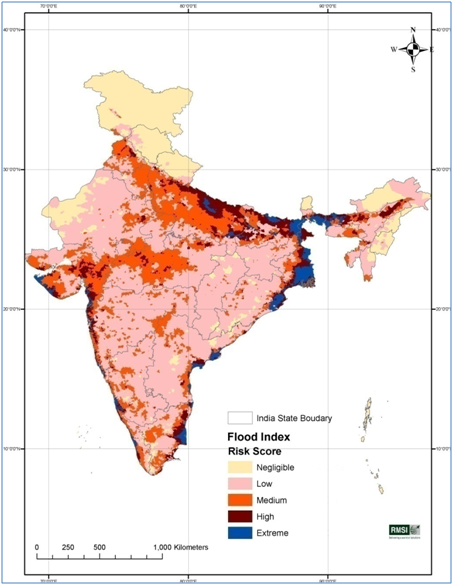

Using probabilistic NatCat modelling, homogeneous risk zones could also be created , that associate hazard intensities to average losses within every homogeneous zone and provides a hazard risk score. Specific rates could be developed by risk zone for taking into account the NatCat risk in pricing of policies. Figure 2 shows the flood hazard risk score zones. This could serve as a basis for the definition of the triggers for specific areas along with payouts associated to the trigger. For every such homogeneous zone, an authentic source that provides the hazard intensity values at the time of the event will have to be setup to ensure success of parametric insurance. So, NatCat modelling not only helps to setup the triggers and associated payouts but also the number of trigger monitoring stations and areas where these should be setup.

The models

could also be used to test out various insurance penetration scenarios and how

various levels of penetration could impact the risk as well as pricing of the

coverage.

No comments:

Post a Comment